In 2025, the contribution limits for 3rd pillar 3a in Switzerland are set as follows:

- Employees affiliated to a pension fund (2nd pillar) : CHF 7'258.

- Self-employed or persons without pension fund membership : up to 20% of net income, with a maximum of CHF 36,288.

These amounts reduce your taxable income, thus offering significant tax savings. In addition, funds saved in the 3rd pillar benefit from tax exemptions during the savings phase and from reduced taxation when withdrawing.

Respecting the ceilings is essential to maximize these tax benefits. Careful planning, such as splitting withdrawals or using multiple accounts, can also optimize your savings strategy.

Everything you need to know about the 3rd pillar in 2025

Maximum contribution amounts 2025

After discussing the tax benefits associated with the 3rd pillar for 2025, let's look at the maximum contribution amounts. These limits depend on your employment situation and whether you are a pension fund member or not, and they determine the maximum amount you can deduct from your taxes.

Limits for persons affiliated to a pension fund

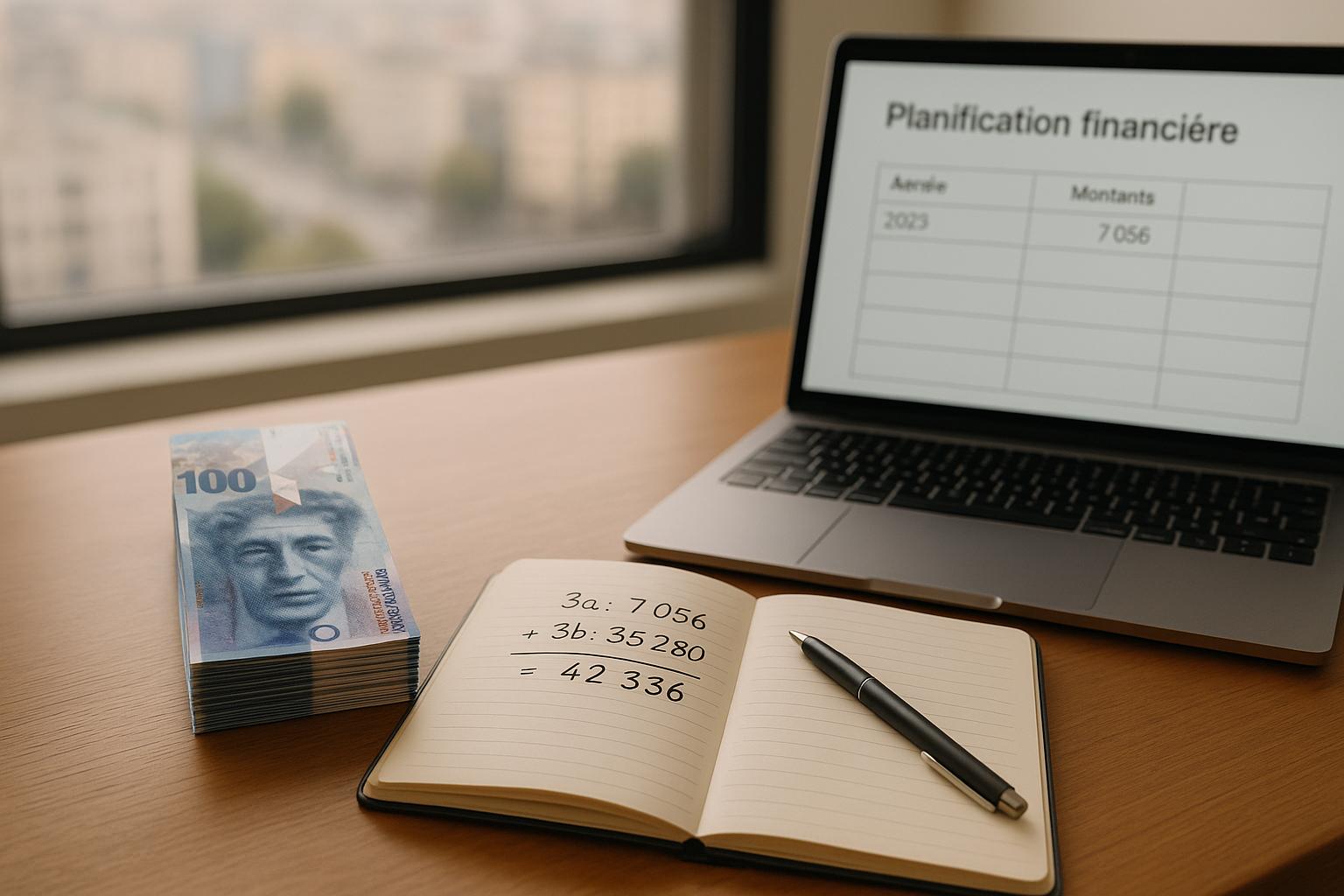

If you are an employee and contribute to a pension fund (2nd pillar), the maximum amount of your 3rd pillar 3a contribution for 2025 is set at CHF 7'258 [4—10]. This amount represents an increase of CHF 202 compared to 2024, when the ceiling was CHF 7,056.

Limits for people without pension fund membership

For self-employed persons and employees not affiliated to the LPP, the ceiling is higher. You can contribute up to 20% of your net professional income, within the limit of an absolute maximum of CHF 36'288 in 2025. For example, if your net income is CHF 200,000, 20% would correspond to CHF 40,000, but you can only deduct up to CHF 36,288.

Here is a summary table to clarify these limits according to your situation:

Summary table of contribution limits

These amounts define the maximum amount that can be deducted on your tax return. Of course, you have the option of contributing a lower amount, but any amount that exceeds these limits will not be taken into account for a tax deduction.

How are contribution limits set

In Switzerland, 3rd pillar ceilings are governed by strict rules defined by the Confederation. These limits are revised regularly according to the criteria established by the legislation in force.

Link with AVS and LPP maximums

The contribution limits for pillar 3a depend directly on the amounts set for AHV and occupational benefits (BVG/LPP). Their calculation is based in particular on the maximum insured salary under the compulsory regime and on the maximum AHV pension. For 2025, the Federal Council has set this pension at CHF 30,240 per year, or CHF 2,520 per month. This mechanism allows the ceilings to be automatically adjusted according to changes in wages and the cost of living.

For example, the ceiling of CHF 7,258 for persons affiliated to a pension fund corresponds to around 24% of the maximum annual AHV pension. This structural relationship explains why ceilings change regularly, as illustrated below.

Historical evolution of contribution limits

Periodic ceiling reviews play a key role in financial planning. In general, these amounts are adjusted every two years by the Federal Council in accordance with the Ordinance on Occupational Old-Age, Survivors and Disability Insurance (OPP 3). This biennial rhythm makes it possible to take account of economic developments while avoiding excessively frequent changes, which could complicate the procedures of taxpayers.

Sbb-ITB-505FA4B

Tax benefits of maximum contributions

The 3rd pillar offers attractive tax opportunities, whether during payments, during the savings phase or when withdrawing. These advantages make it a valuable tool for structuring and optimizing your pension provision, taking into account the contribution limits mentioned above.

Tax reduction thanks to contributions

Contributions paid into a 3rd pillar account (pillar 3a), within the limits of the ceilings set for 2025, directly reduce taxable income. This results in an immediate reduction in tax liability, depending on your tax bracket. If you are not affiliated to a 2nd pillar, the higher contribution limit gives you an even greater tax advantage.

Tax-free growth during the savings phase

In addition to the immediate tax deduction, pillar 3a ensures that the funds saved grow without being subject to taxes on wealth, income, interest or capital gains. This mechanism favors the effect of compound interest, thus accelerating the growth of your savings. In some cantons, the wealth tax exemption can represent an annual saving of between 0.1% and 1.0%, an advantage that accumulates as long as the funds remain invested.

Attractive taxation upon withdrawal

When you withdraw Pillar 3a funds, they are subject to a specific tax on capital benefits, calculated at federal, cantonal and municipal levels. This rate is significantly lower than that of ordinary income tax, often equivalent to about a fifth of the standard rate. However, this tax is progressive: the higher the amount withdrawn, the more the applied rate increases. A good strategy is to plan your withdrawals over several years in order to reduce the impact of this progressiveness. It is also important to note that simultaneous withdrawals from pension funds (2nd pillar) and 3rd pillar accounts, made in the same fiscal year, are taken into account together for tax calculation.

In the next section, we'll look at how to take advantage of these tax benefits to maximize your 3rd pillar savings.

How to make the most of 2025 contribution limits

To maximize your tax deductions and grow your savings, thoughtful contribution planning is essential. How you structure your payments can have a significant impact on long-term results.

When to make your payments

Once you know the contribution limits, it becomes crucial to choose the right time to make your payments. By paying the amount at the beginning of the year, for example in January, you benefit from increased capitalization. Compared to a payment made at the end of the year, this choice can generate a significant additional return. If you can't pay in full at once, opt for monthly payments. This approach not only smooths out market variations, but also allows you to manage your budget in a more balanced way.

Benefits of opening multiple 3a accounts

Having several pillar 3a accounts can be a smart strategy, especially in terms of taxation. This makes it possible to spread your withdrawals over several years, thus reducing the impact of tax progressiveness. This method can also simplify the management of your estate. By staggering your withdrawals, you potentially reduce the total amount of taxation, while adapting this approach to your savings and your local taxation.

Investing with pillar 3a

3a investment accounts give you access to a variety of assets, such as stocks, bonds or real estate. These options allow you to diversify your investments and reduce risks, especially if you have a long-term investment horizon. A simple rule is to adjust the share of stocks in your portfolio according to your age and risk tolerance. These investment strategies complement your contributions, helping you optimize your savings for the future.

Use custom planning tools

To get the most out of your contribution plan, a tailor-made financial analysis is essential. Each situation is unique, whether in terms of income, retirement goals, or tax constraints.

The platform Best Third Pillar provides you with tools to refine your strategy. You can track your annual contributions, compare the options available, and assess the associated fees. In addition, free consultations with experts are offered to adjust your plan according to changes in your personal or professional situation. With annual monitoring, you can adapt your strategy in the face of fiscal or personal changes, thus guaranteeing an optimized approach that is well integrated to your needs.

Conclusion

Les 2025 contribution limits represent a great opportunity to maximize your retirement savings while reducing your tax burden. Whether you are an employee affiliated with a pension fund or a self-employed person, knowing these limits well and knowing how to incorporate them into your planning can make all the difference.

Everything is based on a approach adapted to your personal situation. Your retirement goals, professional status and taxation must be taken into account in order to define a tailor-made strategy. Fortunately, practical tools are available to support you in this process.

For example, Best Third Pillar offers free simulation tools. These tools help you estimate your tax savings, compare different options, and adjust your plan according to your needs and changing circumstances.

In summary, 2025 offers interesting opportunities to optimize your finances. Understanding contribution limits and thoughtful planning can strengthen your financial security in the long run.

FAQs

How can I optimize my tax savings with 3rd pillar 3a in 2025?

To reduce your taxes in 2025 thanks to the 3rd pillar 3a, it is a good idea to pay the maximum authorized amount. In 2025, this amount rises to CHF 7,258 for employees and to 36,288 CHF for self-employed persons not affiliated to a pension fund. These contributions are fully deductible from your taxable income.

By paying these amounts, you could significantly reduce your tax bill. Depending on your personal situation and the canton where you live, the savings can represent up to 48% of the amount paid. It is a solution that combines two major advantages: saving for your retirement while benefiting from an immediate tax reduction.

What are the benefits of having several 3rd pillar accounts to optimize my savings in Switzerland?

Having several 3rd pillar accounts in Switzerland can be a smart strategy to reduce the tax you pay when withdrawing your funds By spreading withdrawals over several years, you limit the effect of progressive taxation, which increases with the amount withdrawn.

In addition to this tax advantage, dividing your contributions across several accounts can offer you a valuable flexibility in the management of your savings. This not only allows you to optimize your annual tax deductions, but also to make the most of the tax advantages over the long term.

When is it best to pay my 3rd pillar contributions in Switzerland?

To get the most out of your 3rd pillar in Switzerland, it is a good idea to start contributing as soon as your financial situation allows it. By acting early, you benefit from the effect of compound interest, which allow your savings to grow over the long term.

It is also important to make your payments before the end of the fiscal year. This allows you to take advantage of tax deductions on your income for the current year. You have the freedom to choose between regular contributions or a one-time payment, depending on your preferences and financial situation. This choice can adapt to income fluctuations or changes in your tax rate.

By carefully planning your contributions, you can not only maximize your tax savings, but also consolidate your retirement savings.