With its tax advantages, returns and retirement savings, the 3rd pillar is one of the most reliable ways to sustainably strengthen your financial security. Avec ses avantages fiscaux, ses rendements et son épargne retraite, .

Lower your taxes

The 3rd Pillar reduces income tax, exempts your capital from wealth tax, grows your savings and lightens your tax burden from today.

Secure your retirement

Only 60% of your retirement income covered by AVS and LPP? Increase your income, use your 3rd pillar to invest or become a homeowner and prepare for a more flexible retirement.

Insure against the unexpected

Capital paid to your loved ones in the event of death, guaranteed income in the event of disability, exemption from premiums in the event of incapacity and guaranteed capital depending on the type of 3rd pillar.

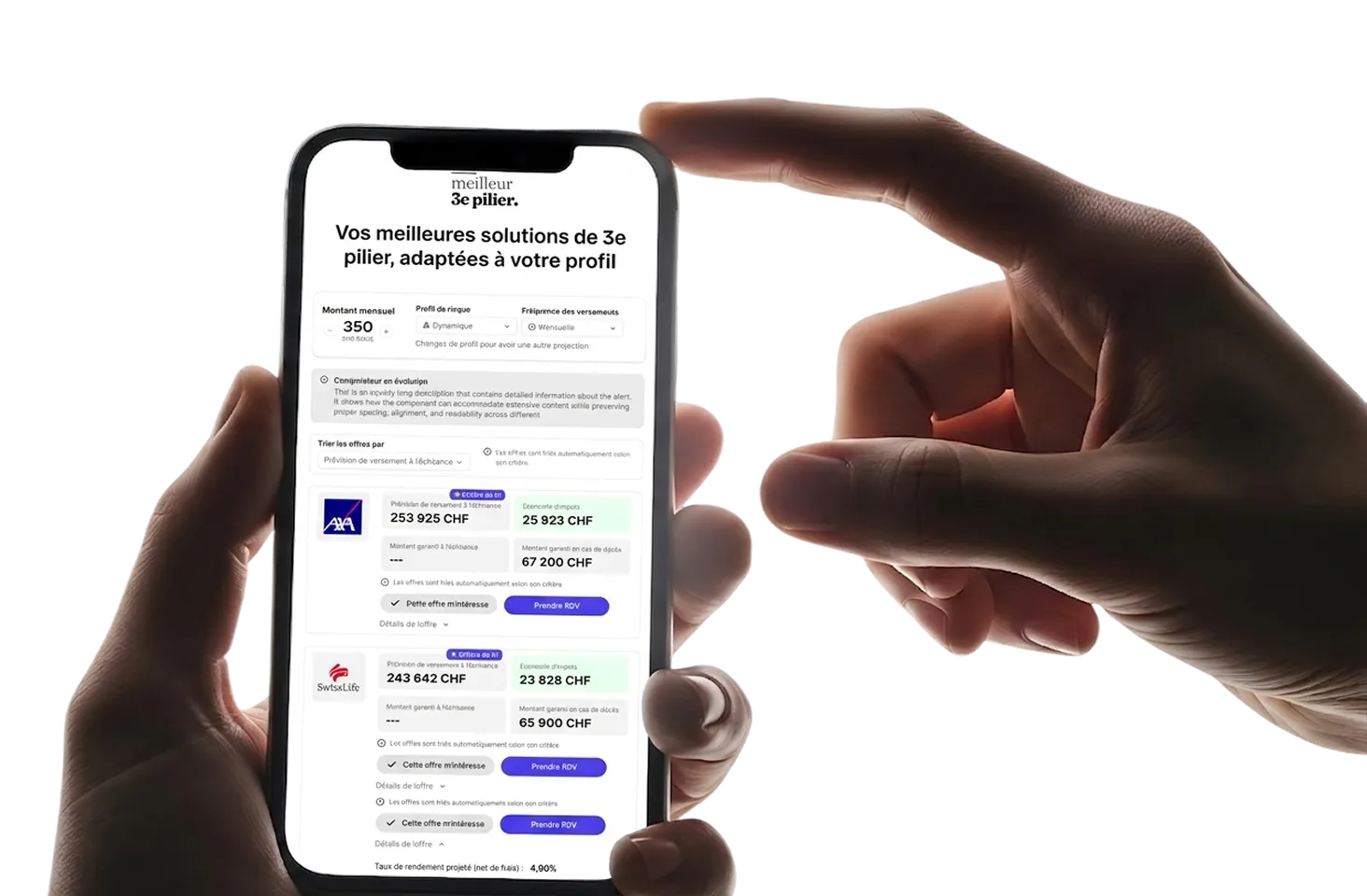

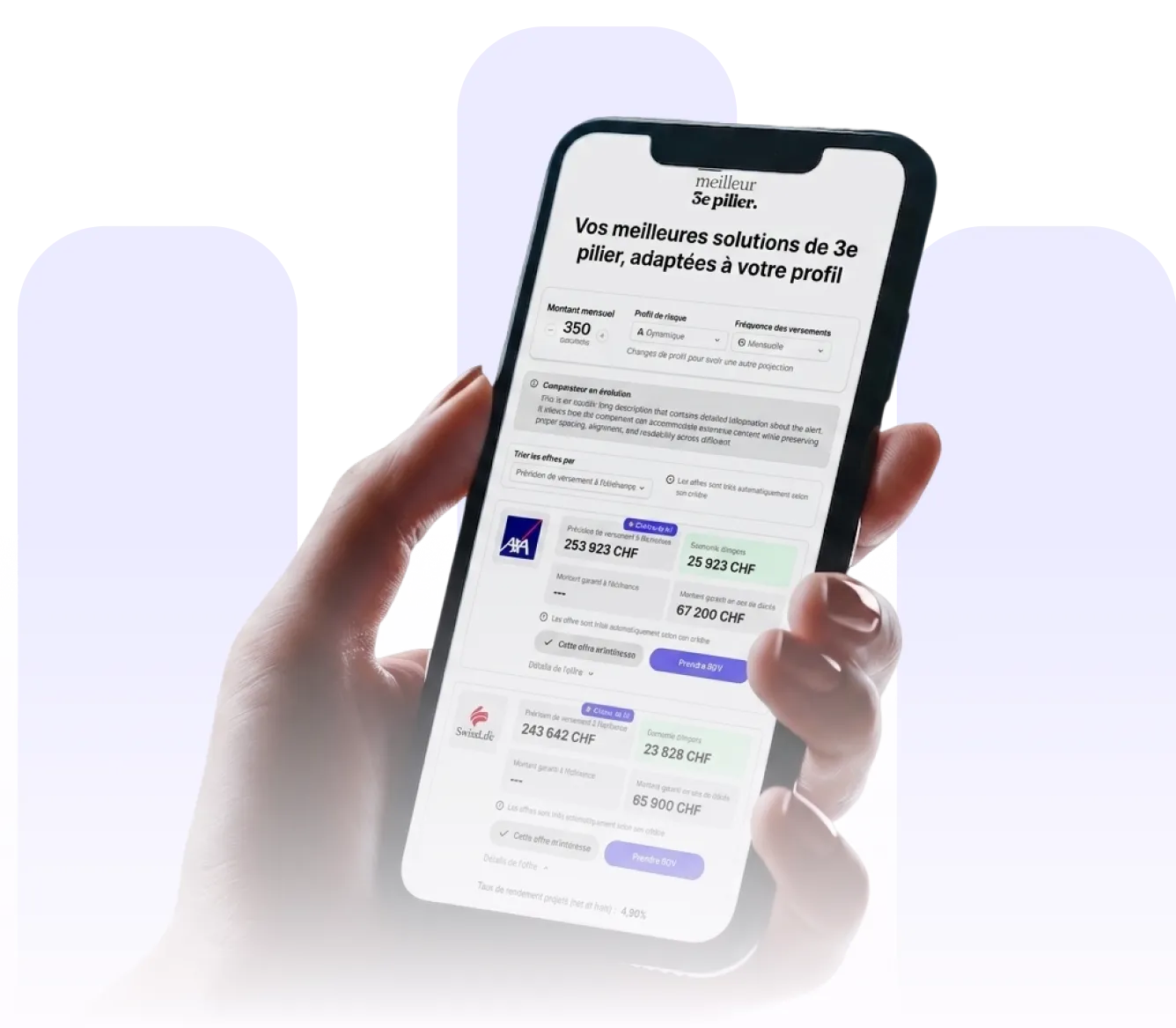

Analysis of your profile and transparent comparison of your 3rd pillar options

A personalized analysis, objective advice and continuous monitoring to optimize your 3rd pillar.

Analysis Analysis of your situation

Estimates of your retirement pensions, recommendations tailored to your status (employee, self-employed, LLC manager). Simulation of tax benefits based on your place of residence (canton, municipality, or cross-border worker status). Optimization of your savings and disability protection, assessment of your pension needs (3rd pillar, disability insurance). Precise calculation of taxation upon withdrawal of your pension capital.

Continuous monitoring and optimization

Transparent explanation of conditions and fees, annual follow-up to adjust your strategy and assistance to optimize your tax return.

Advice and comparison

Comparison of 3rd pillar A vs 3rd pillar B, selection between banking or insurance solution, adaptation according to your objectives and assessment of your gaps in case of disability or death.

Find the best 3rd pillar offer

Depending on your profile and objectives, get your personalized comparison in minutes.

+6000 satisfied customers — 4.9/5 based on +700 Google reviews.

Excellent 4.7sur 5

Trustpilot

4.7 sur 5

5.0 sur 5

« I'd heard about the third pillar but didn't know where to start. In just 3 minutes, I ran a simulation and discovered I could save over CHF 12,000 on my taxes. Excellent service, very personal and clear. »

« I have been putting off the question of the 3rd pillar for years. Thanks to this site I had a clear answer to my needs. The personalized simulation allowed me to visualize the tax savings, and the support afterwards was professional, without bla-bla. »

« Fantastic experience! The simulation is fast, the language is easy to understand, and above all, there's no sales pressure. I was able to ask questions, compare several solutions, and choose the best option for me. »

« J’avais entendu parler du 3e pilier mais je ne savais pas par où commencer. En 3 minutes j’ai fait ma simulation et j’ai découvert que je pouvais économiser plus de 12 000 CHF sur mes impôts. Service au top, très humain et très clair. »

« Je repoussais depuis des années la question du 3e pilier. Grâce à ce site j’ai eu une réponse claire à mes besoins. La simulation personnalisée m’a permis de visualiser l’économie d’impôts, et l’accompagnement ensuite était pro, sans bla-bla. »

« Super expérience ! La simulation est rapide, le langage est simple à comprendre, et surtout on ne sent aucune pression commerciale. J’ai pu poser mes questions, comparer plusieurs solutions, et choisir la meilleure formule pour moi. »

By clicking on”Accept all cookies“, you agree that cookies may be stored on your device in order to improve site navigation, to analyze the use of the site and to contribute to our marketing efforts. Check out our privacy policy for more information.

.png)