The 3rd Swiss pillar is a key solution for preparing for retirement while reducing taxes. In 2025, pillar 3a contributions remain capped at 7'258 CHF per year, offering significant tax advantages. However, choosing the right account depends on several criteria: management fees, investment strategy, ease of use and specific needs (especially for cross-border workers).

Summary of the options analyzed:

- Best Third Pillar : Personalized support, free advice, tax simulation.

- Finpension 3a : Reduced fees (0.39% annual), automated management, international diversification.

- VIAC : Intuitive interface, passive management, personalized strategies.

- Frankly : Security of a cantonal bank, digital management.

- Cornèrbank SA : Guaranteed fixed rate (0.80%), no management fees, secure savings.

Quick recommendations:

- Autonomous investors : Finpension 3a or VIAC for low fees and potential returns.

- Careful savers : Cornèrbank SA for its stability or frankly for its flexibility.

- Need advice : Best Third Pillar, ideal for a tailor-made approach.

Quick comparison:

Conclusion : The choice of account depends on your risk tolerance, tax goals and investment horizon. Take the time to compare options to maximize your retirement savings.

Everything You Need to Know About the 3rd Pillar in 2025

1. Best Third Pillar

With its attractive tax advantages, this account is distinguished by a personalized approach and free advice, specially designed for cross-border commuters and foreign residents. The platform analyzes your tax situation and your retirement goals before offering you the most appropriate solutions.

Cost structure and clarity

The platform provides a Free Simulation Who estimates your potential tax savings and projects your retirement capital. This simulation takes into account the contribution limit of 604 CHF per month, or 7,258 CHF per year for pillar 3a. The fees are explained in a clear manner, so you know exactly what you are paying for. This transparency provides informed decision-making.

Tailor-made consulting services

Les Free consultations with experts Offer an in-depth analysis and recommendations adapted to your situation. You also benefit from a detailed comparison between pillar 3a and 3b options. This is particularly useful for cross-border commuters, who have to juggle the Swiss and French tax systems.

Flexibility and support

The service includes a Annual Follow-up To adjust your financial strategy according to your needs and regulatory changes. In addition, tax filing assistance simplifies your administrative procedures, saving you time and energy.

Specific advantages for cross-border commuters

Cross-border workers benefit from dedicated expertise that assesses the fiscal impacts in both countries and proposes optimized strategies to manage this complexity.

Thanks to a combination of free advice, personalized support and continuous follow-up, this service is a wise choice to prepare for your retirement with complete peace of mind.

2. Finpension 3a

After presenting the best 3rd pillar account, let's look at a digital solution that stands out: Finpension 3a. Unlike a personalized approach, this platform connects on automation and broad diversification to optimize your retirement savings. By relying on index funds, it adopts a strategy Passive That reduces costs while maximizing long-term return opportunities through international diversification.

Competitive and transparent fees

With fees set at 0.39% per year, Finpension is positioned among the most economical options. For a capital of 50,000 CHF, this represents approximately 195 CHF per year. This transparency makes it possible to better anticipate the impact of costs on your savings, a crucial point for effective financial planning.

A Range of Investment Strategies

The Platform Offers Five Investment Strategies, adapted to different risk profiles. You can choose from portfolios ranging from a conservative model (20% shares) to a fully dynamic model (100% shares). These strategies are based on ETF index funds Renowned managers such as Vanguard And iShares, guaranteeing diversified exposure on a global scale. This approach reduces risks while increasing the chances of growth.

Quick and easy account opening

Opening an account is done entirely online in Less than 10 minutes. After a short questionnaire to assess your risk profile, your portfolio is set up automatically. You then have the freedom to schedule monthly payments or to make them according to your preferences.

Automated Management and Rebalancing

Thanks to Automatic rebalancing, your portfolio remains aligned with the defined target allocation. In the event of market fluctuations, Finpension automatically adjusts the distribution between shares and bonds to maintain the initial strategy. This passive management protects you from impulsive decisions during periods of volatility.

Points to note for border residents

Cross-border residents can also benefit from Tax deductions, with an annual limit set at CHF 7,258. However, the platform does not offer specific tax advice for cross-border situations. It is therefore recommended that you consult a tax expert to optimize your situation in both countries.

Finpension is an ideal solution for those looking for simple, economical and efficient management of their 3rd pillar, without requiring personalized support.

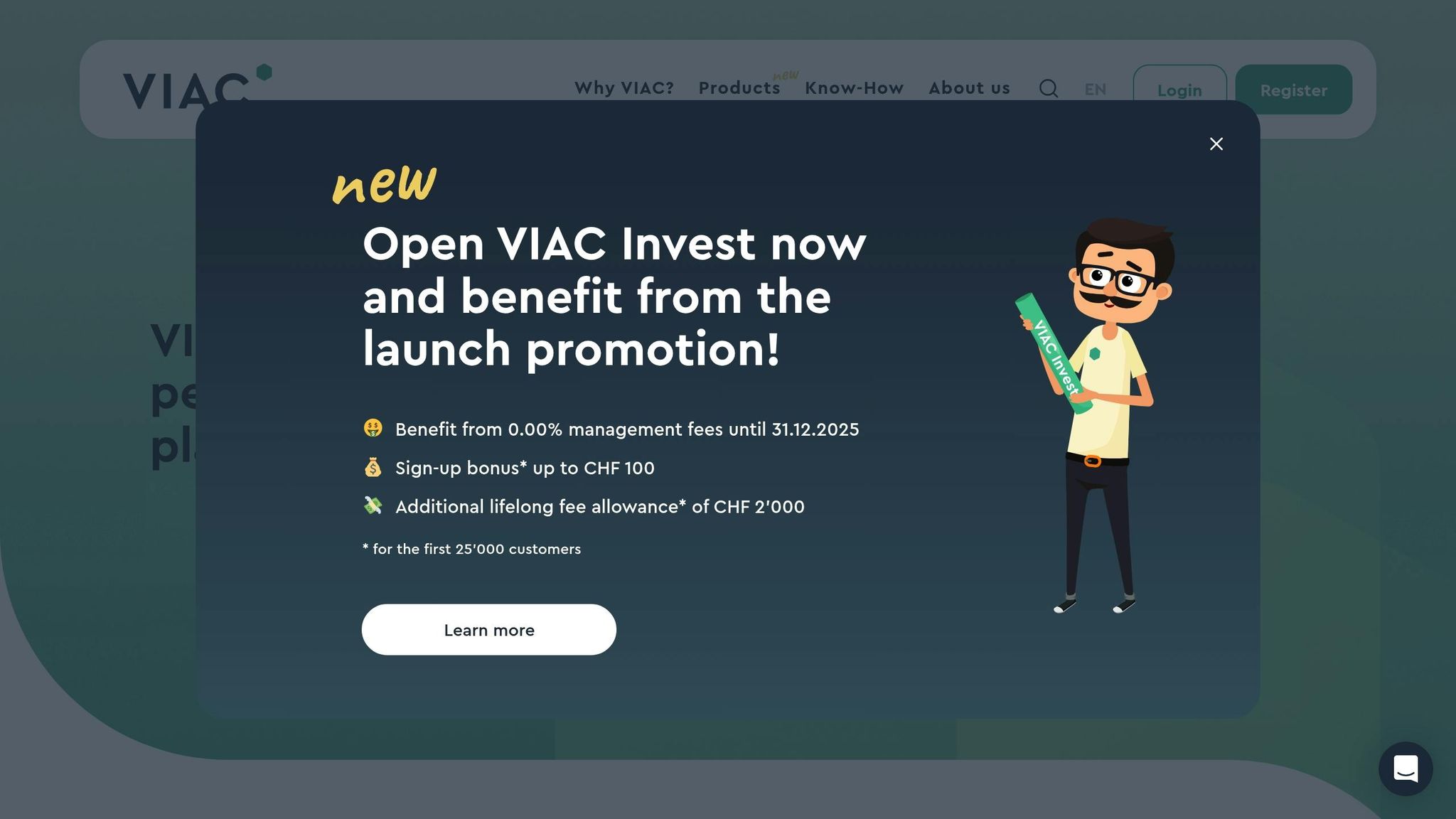

3. VIAC

Let's continue our exploration with VIAC, a platform that combines advanced automation and personalization in 3rd pillar management. It stands out for its modern approach and flexibility.

Transparent and competitive fees

VIAC offers a simple and clear pricing structure. No hidden fees or surprise commissions, making it an attractive option for effectively managing your 3rd pillar.

Customized investment strategies

Whether you prefer a cautious approach or are ready to take more risks, VIAC offers strategies adapted to different profiles. These are based on carefully selected ETFs, guaranteeing diversification to better manage risks and aim for long-term growth.

An interface designed for the user

Registration is entirely online, and your wallet is automatically set up according to your profile. The intuitive interface allows you to monitor your investments in real time, making management simple and accessible.

Automatic rebalancing

To maintain the consistency of your portfolio, VIAC automatically adjusts the target allocation according to market fluctuations. This ensures optimized management without additional effort on your part.

Flexible payouts

VIAC adapts to your financial needs by accepting both one-off and regular payments. This flexibility is suitable for a variety of saver profiles and financial situations.

A solution for cross-border commuters

Cross-border workers can also take advantage of the tax advantages linked to the 3rd pillar thanks to VIAC. The platform accepts some residents from neighboring countries, thus expanding access to its services. However, to maximize these benefits, it is advisable to consult a tax specialist, as mentioned earlier, in order to optimize your situation.

4. Frankly (Zürcher Kantonalbank)

Now Let's Move On To Frankly, the digital solution from Zürcher Kantonalbank that modernizes the 3rd pillar thanks to an elegant and intuitive digital interface. This platform combines the reliability of a well-established cantonal bank with a digital approach designed for today's users.

A traditional bank in the digital age

With Frankly, You Get the solid banking expertise of Zürcher Kantonalbank, one of the most respected financial institutions in Switzerland. This base offers reassuring security for your retirement savings, while integrating modern tools for simplified management.

Transparent Fairies

The pricing structure is clear and depends on the investment strategy chosen. This allows for predictable financial management that is tailored to your long-term goals.

Personalized Investment Strategies

Frankly Offers a Range of Investment profiles That adapts to your risk tolerance. These diversified portfolios are based on index funds, offering a balance between performance and security to prepare for retirement.

An interface designed for simplicity

Account opening is entirely digital. Once your profile is created, the Automatic rebalancing Ensures that your portfolio stays in line with your investment goals.

Flexible payouts

Whether you prefer Regular or One-Off Payments, frankly adapts to your financial situation to offer you optimal flexibility.

An option for cross-border commuters

If you are a cross-border worker or a foreign resident, it is essential to check your eligibility and to ensure that this account meets your specific needs, especially in tax matters. A consultation with a specialized tax advisor can be useful in order to maximize the benefits of your retirement savings.

These elements enrich our comparative analysis and prepare the ground for a more detailed assessment of the strengths and limitations of this solution.

5. Cornèrbank SA

Cornèrbank SA offers Cornèr3, a 3rd pillar savings account designed for those who value security and simplicity. This product differs from solutions investing in the stock market by offering a stable and predictable alternative. Ideal for savers who want to avoid financial market fluctuations.

An account with no management fees

Cornèr3 stands out for the absence of management fees. This particularity allows you to keep all of your savings to optimize your retirement savings over the long term.

A competitive interest rate

With a Interest rate of 0.80%, Cornèr3 guarantees stable growth in your economies. This rate, fixed upon opening, remains unchanged despite market variations, thus offering peace of mind.

A conservative and risk-free solution

Unlike accounts linked to investments in securities, Cornèr3 excludes any acquisitions of stock market assets. This means there are no fund management fees, making it an ideal option for those who prefer to avoid the vagaries of the market.

Tax benefits maintained

Cornèr3 offers the same tax benefits as other 3rd pillar solutions. Your payments are Deductible from taxable income, interest is not subject to withholding tax, and capital is taxed at a reduced rate upon withdrawal.

Limited accessibility

It is important to note that access to Cornèr3 is subject to regulatory restrictions. This may limit its openness to foreign residents or cross-border workers depending on their situation.

Information for cross-border workers

Cross-border workers must check their eligibility before subscribing. The application forms are mostly available in German, although registering online is still a convenient option.

One-off costs to consider

Although Cornèr3 does not charge management fees, some occasional fees may apply, especially for early withdrawals or transfers. However, these costs remain modest compared to the recurring costs of other solutions.

Cornèr3 is particularly suitable for savers looking for a simple and secure solution, although the return is lower than that of more diversified options. This approach focuses on stability and predictability, ideal for managing retirement savings calmly.

Sbb-ITB-505fa4b

Advantages and disadvantages

Each option has advantages and limitations that can meet different needs and profiles.

To better understand, here is a summary of the main benefits and limitations of each option.

Strengths of each solution

- Best Third Pillar : Provision of an expert advisor and free simulation to maximize your tax savings.

- Finpension 3a : Very competitive management fees and broad diversification of investments.

- VIAC : High return potential with a modern interface to monitor your investments.

- Frankly : Reliability of Zürcher Kantonalbank and flexibility with monthly payments.

- Cornèrbank SA : Increased security thanks to a guaranteed fixed rate and no management fees.

Things to Watch Out for

- Some solutions involve a risk linked to market fluctuations, with no guarantee of future performance.

- Cross-border workers may face access restrictions depending on where they live.

- Additional fees or tax procedures may be required when making withdrawals or transfers.

These things should be taken into account before making your choice. Here are some recommendations adapted to different profiles.

Recommendations according to your profile

- Young professionals (25-35 years old) : VIAC And Finpension 3a Stand out for their long-term growth potential and flexibility.

- Experienced savers (35-50 years old) : Best Third Pillar is ideal for optimizing your tax deductions and structuring your investments.

- Prudent profiles or close to retirement : Cornèrbank SA And Frankly Offer increased security with stable returns.

The final choice depends on your age, risk tolerance, tax situation, and retirement goals. The following sections will guide you to an informed decision.

Final recommendations

After considering the various options, here are our tips for choosing the 3rd pillar that fits your needs and goals.

To optimize your tax savings while benefiting from personalized follow-up, Best Third Pillar is distinguished by an approach focused on your specific needs. This tailor-made support can maximize your tax benefits, as mentioned earlier.

If you prefer reduced fees and broad diversification, Finpension 3a is ideal for self-employed investors looking to minimize costs while diversifying their portfolio.

For high potential performance combined with a modern interface, VIAC Is a great choice for tech-savers. This solution combines intuitive management with a focus on long-term growth.

Profiles That Are More Cautious or Close to Retirement Might Prefer Cornèrbank SA, which offers guaranteed fixed rates with no management fees, or Frankly, offering the security of Zürcher Kantonalbank with the flexibility of monthly payments.

Beware of restrictions for cross-border commuters : some solutions impose limitations depending on where you live. Please check the access conditions before you sign up.

Finally, the amount you want to invest also plays a role. For example, Cornèrbank SA Requires a larger initial deposit, while other options, such as VIAC or Finpension, allow for more flexible amounts.

Take the time to assess your risk tolerance, investment horizon, and advice needs before making your choice. These recommendations aim to guide you towards the 3rd pillar account that best suits your situation.

FAQs

What priority elements should be considered when choosing a 3rd pillar account in 2025?

How to choose the best 3rd pillar account in 2025?

To select the 3rd pillar account that best fits your needs in 2025, several criteria deserve your attention:

- Contribution limit : Employees affiliated to a pension fund can pay up to CHF 7'258 Per year, while self-employed persons without a pension fund can contribute up to CHF 36'288.

- Tax reduction : The amounts paid are deductible from your taxable income, which directly reduces your annual tax burden.

- Investment options : Analyze the proposed solutions. Some accounts offer a wide range of investments, such as index funds or diversified portfolios, adapted to different risk profiles.

- Ease of Management : Opt for an account that simplifies your procedures, in particular to adjust your contributions or optimize your tax benefits as you approach retirement.

Remember to take into account specific needs, such as those of cross-border commuters or foreign residents, and to carefully review the fees applied. These elements can influence your long-term returns and maximize your savings.

How can cross-border workers make the most of the 3rd pillar while managing the tax implications between Switzerland and France?

Cross-border workers and the 3rd pillar: a retirement savings opportunity

Cross-border workers can take advantage of the 3rd pillar Switzerland To optimize their retirement savings, while benefiting from attractive tax advantages in Switzerland, provided they benefit from the status of virtual resident. In addition, when the capital is withdrawn, it is subject to reduced taxation set at 6.75%.

However, it is important to note that in France, these tax deductions are not systematically recognized. This can lead to double taxation situations if accurate tax planning is not put in place. To avoid such inconveniences and maximize the benefits of the 3rd pillar, it is strongly recommended to consult a specialist. The latter can help you develop a strategy adapted to your situation, while respecting the tax obligations of both countries.

What are the tax advantages of the 3rd pillar in Switzerland and how can you make the most of them?

The 3rd pillar and its tax advantages in Switzerland

The 3rd pillar in Switzerland allows you to benefit from Attractive Tax Cuts, in particular by deducting your contributions from your taxable income. For the year 2025, the maximum deductible amount is CHF 7,258 for employees affiliated to a pension fund. For the self-employed, this ceiling rises to 36,288 CHF.

In order to make the most of these benefits, it is advisable to contribute the maximum amount allowed each year. If you did not reach these limits in previous years, you have the option of making up for these contributions with retroactive purchases. This not only allows you to increase your tax deductions, but it also allows you to strengthen your savings for retirement.